7 Dos and Don’ts of Financial Management for Startups

Building a startup from the ground up is one of the most difficult things for an entrepreneur. The road to a successful startup is rocky and often filled with insurmountable challenges. Establishing a strong financial infrastructure is crucial for startups. Yet, it’s often an afterthought for most rookie entrepreneurs. Despite having a compelling business model, the most common reason why many startups fail is due to the cash crunch and unwise financial management.

If you’re an entrepreneur who has just started out and are entangled in financial complexities, here are some financial management tips that can help you in the journey.

Financial Advice for Entrepreneurs

Don’t: Avoid hiring an accountant

Do: With all the expenses of starting a new business piling up, hiring an accountant may not seem that urgent. After all, you might think that you can keep on top of things.

However, as a busy entrepreneur, bookkeeping and accounting are bound to take a backseat. A regular record of cash inflows and outflows allows you to monitor and manage your money efficiently. Staying on top of your cash flow allows you to monitor your spending and allocate your resources efficiently. It will also enable you to protect your future cash flows, expenses, and revenues. Even if you do not want to hire a full-time accountant, it’s important to have your books prepared and audited regularly by a freelance accountant or an accounting firm.

Don’t: Wait till you start earning money

Do: Financial management must start from the day your company comes into existence. A cash-flow surprise can have a devastating effect on your startup. So, instead of waiting for your startup to become BIG, ensure that you lay the foundation of efficient financial management right from the start to enable your organization to become a data-driven operation that can make better, strategic decisions.

Don’t: Spend more than you make

Do: A solid business plan should include a stable budget. In the beginning, it’s important to keep your expenses low to ensure longevity. Instead of spreading yourself too thin with an elaborate office and other expenses, focus on keeping your fixed expenses within the budget initially. Allocate a majority of the capital to growth and revenue generation.

Don’t: Mix business and personal finance

Do: Mixing personal and business finances can have a crippling effect on finances. It can complicate your financial life and create a problem of personal liability. Late loan and credit card payments can hurt your personal credit score. It’s best to keep a separate account for dealing with business revenues and expenses. Use a separate credit card for handling business finances and make sure that you record the expenses that arise out of using personal assets for the business.

Don’t: Forget to review your performance

Do: Once you’ve established measurable and reachable financial goals, it’s important to review your performance regularly, on a monthly, weekly and even daily basis. This will allow you to stay on track, plan for continuing expenses and be prepared for emergencies such as loss of key personnel, equipment failure, etc.

Don’t: Forget to pay yourself

Do: A common mistake startup owners make is to pay themselves. You should keep a specified amount that you should withdraw from the business account to pay for your personal and household expenses. This will not only ensure that your personal finances remain sound but would also ensure that the profit and loss statements of the business are not affected and there is clarity and proper maintenance of your accounts.

Don’t: Miss out on technology

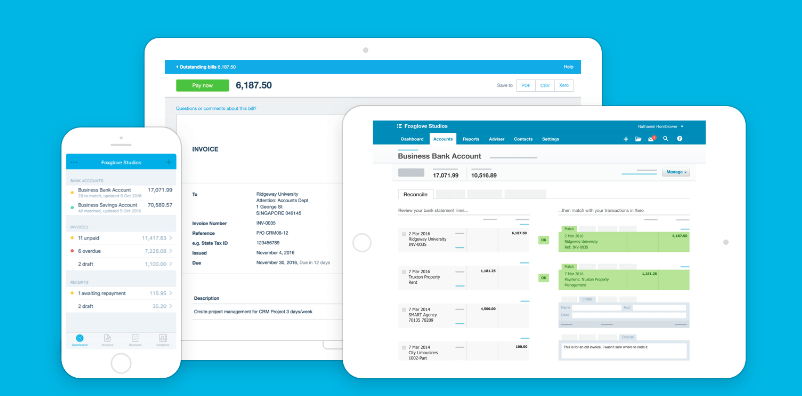

Do: For cash-strapped businesses which cannot afford to hire accountants, small business accounting software such as QuickBooks, ProfitBooks, Xero, Tally ERP.9, and Zoho Books, are the best options for managing your money. These tools have an easy-to-use interface that allows small business owners to manage their invoices, get paid, accept payments and much more.

Entrepreneurs from a non-financial background who are clueless about financial management can enroll into online courses. These courses demystify the basics of accounting and finance, including budgeting, balance sheets, statement of cash flows and income statements, among other things.

As the owner of a fledgling new business, tell us about the financial challenges that your business has faced?